A veterinary specialty practice owner in Minneapolis had two checks arriving each month during her shoulder surgery recovery.

One came from the BOE carrier. One came from the personal disability income carrier.

Neither check overlapped with the other. Neither carrier coordinated with the other.

For 9 months, the practice survived on one check. The owner’s household survived on the other.

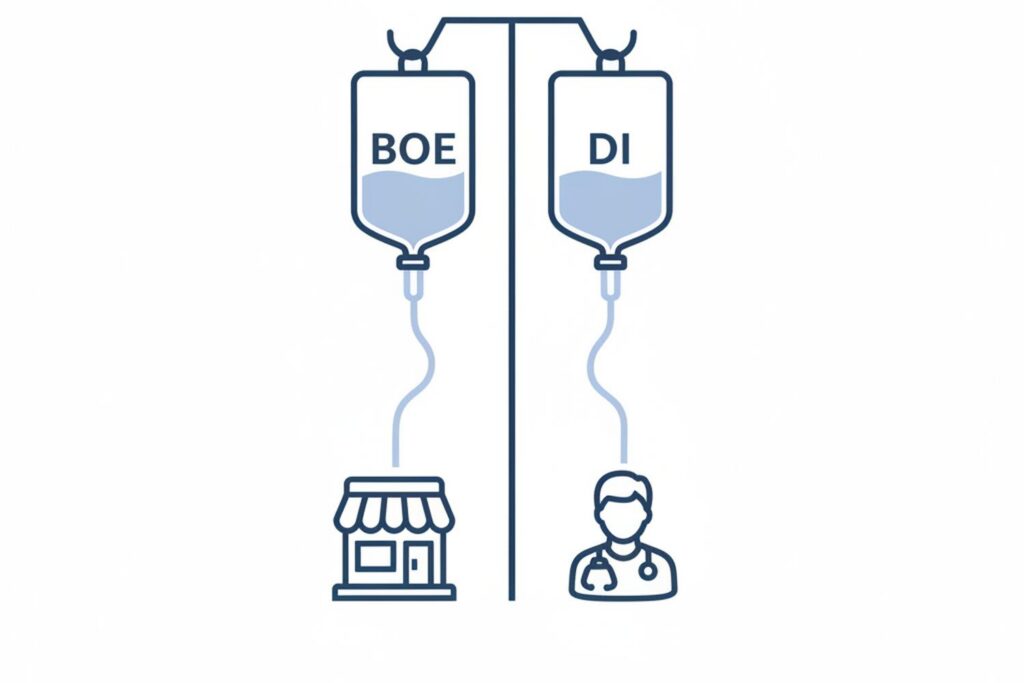

The two-policy structure is the standard pair brokers recommend at policy purchase. Business overhead expense disability insurance alongside a personal disability income policy is the structural design for practice-owner protection.

The two contracts insure two different risks. They pay two different parties.

The carriers underwrite each policy independently. The BOE carrier looks at the practice’s fixed-overhead exposure during owner disability.

The personal disability income carrier looks at the owner’s earning capacity.

The two underwriters can sit at the same insurance company. They are usually two different teams applying two different rate schedules and two different occupation-class tables.

A practice owner with both policies fills out two applications. One paramedical exam covers both carriers, and the owner pays two separate premiums each month.

The two carriers do not offset each other at claim time. The BOE carrier pays the documented reimbursable amount up to the policy’s monthly limit.

The personal disability income carrier pays the contracted monthly benefit on the same disability event.

A vet owner with $8,000 monthly personal disability benefit and $12,000 monthly BOE coverage collects up to $20,000 a month during a covered disability. The personal carrier does not reduce her check because BOE is paying separately.

| Dimension | Business overhead expense (BOE) | Personal disability income |

|---|---|---|

| Who the policy insures | The practice’s fixed overhead | The owner’s earned income |

| Who receives the benefit | The practice (the Owner is default Benefit Recipient) | The owner |

| Premium tax treatment | Deductible as a business expense (IRS Section 162) | Paid with after-tax dollars |

| Benefit tax treatment | Taxable to the practice | Tax-free to the owner |

| Net tax impact during a covered claim | Close to zero (deductible expenses offset taxable benefit) | None (premium was already after-tax) |

| Benefit period | 12, 18, or 24 months | Typically to age 65 or 67 |

| Underwriting | Carrier prices the practice’s fixed overhead exposure | Carrier prices the owner’s lost earning capacity |

The tax treatment differs by policy.

A personal disability income policy paid for with after-tax dollars produces tax-free benefits at claim. The owner takes the benefit check, pays no federal income tax on it, and the dollars retain their full purchasing power.

BOE premiums work the other way. Guardian’s published guidance on business overhead expense protection states the tax treatment plainly. “Premiums for business overhead insurance policies are generally a tax-deductible expense for the business. Benefits paid are taxable to the business; however, the expenses for which the benefits are used for reimbursement are deductible to the business.”

The premium deduction falls under IRS Section 162, the general business-expense provision, and is documented in IRS Publication 535. The practice’s accountant reports the BOE premium on Schedule C for a sole proprietor or on the practice’s form 1120 for an S-corporation.

Because the premium was deductible, the benefit is taxable when the carrier pays the claim. The practice reports the BOE benefit as income and pays expenses out of that taxed income.

The two tax flows are not in tension. Each is the right answer for its product family.

The personal disability income tax flow is intentional. The owner who pays the premium with after-tax dollars is buying tax-free income replacement.

The BOE tax flow is also intentional. The practice that deducts the premium is timing the tax to the moment the benefit arrives.

The deductible expenses the BOE policy reimburses match the taxable benefit dollar for dollar at the practice level. The net tax impact during the disability period is close to zero.

Practice owners often underbuy the personal disability income side of the pair on premium grounds.

The owner shops BOE on her own, finds the rate manageable, and skips the personal policy on the assumption that the practice’s BOE benefits can substitute.

The substitution does not work. BOE pays the practice.

The owner is paid out of the practice’s net cash flow, which is what BOE is making whole in the first place.

The owner without a personal policy receives no monthly income while disabled.

Bob Herum, president of the Council for Disability Income Awareness, framed the carrier’s role during a claim event on the Income Protection Journal Podcast.

“We’re their bank. We’re the only monies that are coming in at this point.”

Bob Herum, president, Council for Disability Income Awareness, on the Income Protection Journal Podcast

The bank is the carrier. For the practice owner who has only BOE, the bank only pays the practice.

The owner’s mortgage and her grocery bill are not on that account.

The pair structure recognizes the line BOE draws. The policy leaves the owner’s salary outside the schedule.

That is by design. The personal disability income policy is the other half of the design.

The pair structure also addresses the timeframe mismatch between the two contracts. BOE pays through the practice survival window of 12, 18, or 24 months.

The personal disability income policy typically pays to age 65 or 67.

Disability events that exceed BOE’s window keep paying the owner. The practice has transitioned, sold, or closed by then, and the owner’s income protection continues.

For disability insurance for small business owners running a single-owner practice, the BOE and personal disability income pair is the structural baseline brokers recommend.

Multi-owner practices add a buy-sell disability policy that funds a partner equity buyout on a permanent disability. The buy-sell policy is the third leg, addressing the partnership equity question that neither BOE nor the personal policy can.

The Minneapolis vet’s 9 months of recovery were not a financial hardship. Both carriers paid on schedule.

The practice kept its lease, its technicians, and its referring relationships.

The owner kept her household running.

The two policies did what the broker had explained at policy purchase. Two contracts, two carriers, one disability event, two checks each month.