Small Business Disability Insurance for Practice Owners and Business Partners

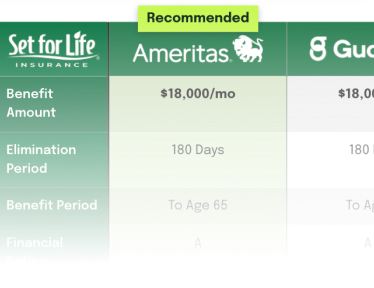

Compare coverage across five carriers.

Small Business Disability Insurance for LLCs, S-Corps and Practice Owners

Small business disability insurance covers the income loss when an owner-operator cannot work. Set for Life Insurance compares own-occupation disability income insurance from Guardian, Principal Financial Group, MassMutual, Ameritas, and The Standard for practice owners and owner-operated practices nationwide. The brokerage has placed coverage for executives and owner-operated practices since 1995. For freelancers, 1099 earners, and other self-employed buyers, see disability insurance for self employed.

Get Your Customized Small Business Quote

Compare Small Business Disability Quotes Side‑by‑Side

"*" indicates required fields

Small Business Disability Insurance Products

Disability Insurance Advantages Reserved for Business Owners

A business owner who buys individual disability insurance can qualify for terms an employee buying the same policy cannot. Carriers reward ownership because an owner’s income, occupation stability, and business assets change the underwriting picture. The result is a higher occupation class, more insurable income, or a lower premium on the same coverage.

The Standard and Ameritas both run a Business Owner Upgrade that moves a qualifying owner up an occupation class, which lowers the premium or raises the benefit on the same policy. The Standard upgrades one class for an owner who holds at least 20 percent of a financially successful business and employs staff. Ameritas upgrades one class for owners in classes 4A through A, and up to two classes with a managerial duties endorsement, when the owner holds at least 20 percent and the business has five or more full-time employees.

Ownership can also raise the amount of income a carrier will insure. The Standard’s Earned Income Enhancer and the Ameritas Business Owner Income Enhancer each let a qualifying owner insure roughly 20 percent more income than a non-owner in the same occupation class, within issue limits, to account for company perks that a salary figure alone does not capture.

Owner-specific and group discounts stack on top of these upgrades. Principal offers a Preferred Business Owner Discount on its buy-out coverage, The Standard a 10 percent Business Owner Discount on its Platinum Advantage policy, and Guardian, Principal, and Ameritas each offer multi-life and association discounts that an owner insuring several people in the business can use.

Every enhancement is subject to underwriter approval and current carrier guidelines, and eligibility turns on ownership share, business tenure, and employee count. Comparing carriers side by side is the fastest way to see which upgrades and discounts a given owner qualifies for.

Occupation Class Structure Showing How Each Carrier Tiers Risk

| Ameritas Life Insurance Corp. Field Underwriting Guide |

Guardian Berkshire Life Insurance Co. of America Provider Choice · IDI Field Underwriting Guide |

MassMutual Massachusetts Mutual Life Insurance Co. Radius Choice · Underwriting Guide |

Principal Principal Life Insurance Company Income Protector · Disability Product Guide |

The Standard Standard Insurance Company Platinum Advantage · Product Guide |

|

|---|---|---|---|---|---|

| Total distinct insurable classes | ~13 | ~14 | ~17 | ~22 | ~12 |

| Top non-medical class | 6A | Class 6 | 5A/5 (with Radius Choice modifier) | 6A+ | 5A |

| Top physician class | 6M | 6M | 5P/1 | 6M | 5P |

| Top dental class | No separate D track, dentists slotted into M classes | 4D | 4D | 4D+ | 3D |

| Lowest insurable non-medical class | B | Class 2 | A | 1A | B |

| Lowest insurable medical class | M | 2M (1M uninsurable) | 3P / 4P (no lower medical class) | 1M | 4P |

| Separate medical-professional track | Yes, “M” classes (6M, 5M, 4M, 3M, 2M, M) | Yes, “M” classes (6M through 1M) | Yes, uses “P” designation (5P, 4P, 3P, 2P) | Yes, “M” classes (6M through 1M, with “+” modifiers) | Yes, uses “P” designation (5P, 4P, 4S, 3P, 2P) |

| Separate dental-professional track | No, dentists assigned within “M” classes | Yes, 4D and 3D | Yes, 4D and 3D | Yes, five-tier dental track (4D+, 3D+, 3D, 2D, 1D) | Partial, 3D only (one combined dental class) |

| Sub-tier or “plus” modifiers between main classes | None | None | Yes, Radius Choice modifiers (5A/5, 5A/3, 4A/3, 4A/2, 4A/1, 5P/1, 3P/2) | Yes, extensive “+” modifiers (6A+, 5M+, 3M+, 2A+, 2M+, 4D+, 3D+) | Limited, 4S (surgeons) is the only intermediate designation |

Source: Field underwriting guides published by each carrier. Class names and product identifiers are taken from the most recently published producer-facing guides held by Set for Life Insurance. Class assignments are subject to underwriter review at the time of application.

Occupation Class Upgrades for Qualifying Business Owners

The occupation class above sets the premium, but two carriers let a business owner improve on the class assigned to the underlying job. The Standard maps earnings and employee count to a target class through its Business Owner Grid. Ameritas raises an owner one class, or two with a managerial duties endorsement.

| Annual earnings | Full-time employees | Resulting occupation class |

|---|---|---|

| $150,000 or more | 10 or more | 5A |

| $100,000 or more | 5 or more | 4A |

| $60,000 or more | 1 or more | 3A |

To use the grid, the owner must hold at least 20 percent of the business, have at least two years of ownership, and perform manual duties less than 25 percent of the time. The grid does not apply to financial advisors, insurance producers, real estate, or entertainment occupations. Ameritas applies its upgrade when the owner holds at least 20 percent of a business with five or more full-time employees.

Among the carriers Set for Life Insurance represents, this occupation-class upgrade is a feature of The Standard and Ameritas. An owner insuring with another carrier is rated on the class of the underlying occupation.

Understanding Small Business Disability Insurance Under ERISA and Section 162

Small business disability insurance addresses a working business owner’s five separate financial exposures during a disability event. These are personal income loss, fixed operating expenses, business loan service, revenue concentrated in a critical employee, and partnership ownership transitions. Each has its own insurance product, its own beneficiary, and its own claim trigger. A single owner with a partnership and a business loan can carry four policies at the same time. The product mix depends on business structure, debt, partner count, and revenue dependencies. The five products coordinate at claim time without overlap.

Personal Individual Disability Insurance

Personal individual disability insurance replaces the small business owner’s income when illness or injury prevents the owner from working. The monthly benefit pays the owner directly, regardless of whether the business continues operating. The owner applies the benefit to personal expenses such as mortgage payments, household costs, and family obligations. Premium is paid with after-tax personal dollars and benefits are received tax-free. Guardian, Principal Financial Group, MassMutual, Ameritas, The Standard, and Lloyd’s of London write individual disability income insurance for small business owners. Profession-specific carrier mix and rider availability are covered on the physician disability insurance, dentist disability insurance, attorney disability insurance, and executive disability insurance landing pages. Owners who recently left a salaried role can often qualify for individual coverage on their prior same-profession earnings, before the new business has two years of tax returns. Several carriers underwrite these newly self-employed applicants on prior W-2 or 1099 income, a path covered in full on the disability insurance for the self-employed page.

Business Overhead Expense Insurance

Business overhead expense insurance reimburses the business for fixed monthly operating expenses while the owner is disabled. Covered expenses include rent, utilities, payroll for non-owner staff, equipment lease payments, professional dues, and scheduled interest on business debt. Premium is deductible to the business and benefits are taxable to the business at payout. Benefit periods are 12, 18, or 24 months, with the maximum monthly benefit decreasing as the benefit period lengthens. Guardian, Principal Financial Group, MassMutual, and The Standard write the coverage. Ameritas does not. Specimen-anchored claim mechanics live on the business overhead expense insurance child page.

Business Loan Protection Disability Insurance

Business loan protection disability insurance funds the principal-and-interest installments on a business loan while the owner is disabled. Covered obligations include practice-acquisition loans, SBA 7(a) and SBA 504 loans, equipment financing, commercial real estate mortgages, and fixed-term loans that rely on the owner’s working capacity. The policy term matches the loan term at issue and shortens as the loan amortizes. Guardian writes Business Loan Protection through Berkshire Life Insurance Company of America; Principal Financial Group writes both a standalone product and a rider variant. Lender requirements and form-ID detail live on the business loan protection disability insurance child page.

Key Person Disability Insurance

Key person disability insurance pays the business when a critical owner, partner, or employee cannot work due to disability. The benefit replaces lost revenue, funds recruiting and onboarding of a replacement, or stabilizes operations during the absence. The insured is the key person; the policy owner and beneficiary is the business. Benefit periods are typically 12 to 24 months, sized to the business interruption window. Premium is not deductible because the policy is treated as a capital expenditure; benefits are generally tax-free to the business. Guardian, Principal Financial Group, MassMutual, Ameritas, and The Standard write key person disability insurance.

Disability Buy-Sell Insurance

Disability buy-sell insurance funds the buyout of a permanently disabled partner’s ownership share. The policy gives healthy partners liquidity to execute the buy-sell agreement without borrowing, depleting business cash, or forcing a sale. The triggering definition of permanent disability is contractually defined in the buy-sell agreement, typically requiring 12 to 24 months of continuous total disability before the buyout obligation starts. The buyout funds as a lump sum, as scheduled installments over 3 to 5 years, or as a combination. Premium is not deductible; buyout proceeds are generally tax-free. Guardian, Principal Financial Group, MassMutual, Ameritas, The Standard, and Lloyd’s of London write disability buy-sell insurance.

When Multiple Policies Pay on the Same Disability Event

A small business owner with multiple disability policies in force may collect on three or four simultaneously. Personal individual disability insurance pays the owner’s monthly compensation. Business overhead expense insurance reimburses the business for rent, payroll, and other fixed expenses. Business loan protection pays the principal-and-interest on the loan. Key person disability insurance pays the business for revenue concentrated in the disabled owner. The four benefits address four separate cost categories. None replaces another. At claim time, each carrier coordinates with the others through the standard Participation Limit established at issue, not at claim.

She made updating my files with each life event stress-free. I watched colleagues struggle to communicate with insurance companies, but not me. One email to Jamie and everything is taken care of. My family is protected and done so with ease, all thanks to Jamie. I highly recommend Set For Life!!!

Disability Coverage by Business Situation

| Triggering business situation | Coverage that addresses it |

|---|---|

| Owner cannot work for 90 or more days | Personal individual disability insurance |

| Fixed operating expenses continue without revenue | Business overhead expense insurance |

| Business loan installments continue regardless of revenue | Business loan protection disability insurance |

| Revenue concentrates in a single owner, partner, or critical employee | Key person disability insurance |

| Partnership disability would trigger a buyout obligation | Disability buy-sell insurance |

Specimen Policies and Carrier Form IDs

| Product | Carrier | Specimen policy form ID |

|---|---|---|

| Personal Individual DI | Guardian Berkshire Life | ICC18 18ID (Provider Choice) |

| Personal Individual DI | MassMutual | Radius Choice (ICC) |

| Personal Individual DI | Principal Financial Group | Income Protector (800 series) |

| Business Overhead Expense | Guardian Berkshire Life | ICC18 18OE (Pub8318 product reference) |

| Business Overhead Expense | Principal Financial Group | ICC25 HH 801 OE (current); HH 789 (legacy) |

| Business Overhead Expense | MassMutual | BOE-99 |

| Business Loan Protection | Guardian Berkshire Life | Pub4371BL Term Rider on ICC18 18OE |

| Business Loan Protection | Principal Financial Group | ICC25 HH 802 BLE (standalone); HH 777 (rider) |

Source: Carrier policy form specimens held by Set for Life Insurance. Form numbers vary by state filing approval and are subject to revision.

Small Business Disability Insurance by Business Structure

Business structure determines which income documentation carriers require at underwriting, who owns the policy, and how premiums and benefits are treated for tax purposes. The five structures common among small business insurance buyers are sole proprietorship, LLC, S-corporation, C-corporation, and partnership. Each produces a different underwriting picture and a different outcome at claim time.

Sole Proprietorship

A sole proprietor and the business are the same legal entity. When a sole proprietor becomes disabled, personal income and business income stop simultaneously. is the only path to income replacement. Carriers underwrite sole proprietor income from two years of Schedule C returns and a current profit-and-loss statement. The maximum monthly benefit is calculated from net Schedule C earnings after the standard half-SECA deduction. Premiums are paid with after-tax personal dollars and are not deductible. Benefits are received tax-free. Guardian, Principal Financial Group, MassMutual, Ameritas, and The Standard write non-cancellable own-occupation coverage for sole proprietors in eligible occupational classes.

LLC

A single-member LLC is a disregarded entity for federal tax purposes and follows the same underwriting path as a sole proprietorship. Income is reported on Schedule C. A multi-member LLC taxed as a partnership distributes income on Schedule K-1, and carriers underwrite the member’s guaranteed payments and distributive share of net income. An LLC owner carrying both personal individual disability insurance and collects two separate benefits during a disability: one replacing personal income, one reimbursing the LLC for rent, payroll, and fixed operating costs. The two policies do not offset each other at claim because they address different loss categories.

S-Corporation

An S-corporation owner who works in the business takes a W-2 salary. Carriers underwrite S-corp owner income from the W-2 salary, not from S-corp distributions. Distributions are return on investment and are not insurable earned income. An S-corp owner who minimizes W-2 salary to reduce payroll taxes also reduces the maximum monthly benefit available at underwriting. The S-corp can pay disability insurance premiums for shareholder-employees who own more than 2 percent of the company, but the premium is included in the shareholder’s W-2 as taxable compensation. Because the premium is taxed on receipt, disability benefits are received tax-free.

C-Corporation

A C-corporation can deduct disability insurance premiums paid for employees under a group plan. For , the most common structure is a Section 162 executive bonus arrangement. The corporation pays the disability insurance premium as a bonus to the executive. The executive includes the bonus in taxable W-2 income and owns the policy personally. Because the premium was taxed, benefits are received tax-free. The policy is portable and follows the executive if they leave the company. A double bonus arrangement increases the bonus to cover the executive’s tax liability on the premium, making the plan economically neutral to the executive. The corporation deducts the full double bonus as a compensation expense.

Partnership

Partnerships face two distinct disability insurance exposures. Each partner needs personal individual disability insurance sized to personal compensation. The partnership also faces a buyout obligation if one partner’s disability becomes permanent under the buy-sell agreement. A two-partner practice commonly carries four policies: one personal income policy per partner and one disability buy-sell policy per partner cross-funding the other’s buyout. Disability buy-sell insurers including Guardian, Principal Financial Group, MassMutual, Ameritas, and The Standard write coverage on an own-and-crossover basis, where each partner owns a policy on the other, or on an entity basis where the partnership owns and funds the policies.