Executive Disability Insurance

Income Protection for Corporate Executives

High Income Disability Insurance

Disability Insurance for High Income Earners

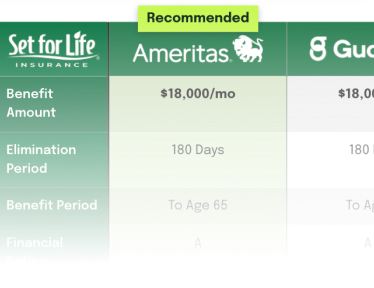

Executive disability insurance provides up to $35,000 per month of own-occupation income protection for executives earning $250,000 to $2 million. Get side by side quotes from Principal, The Standard, Guardian, MassMutual, Ameritas, and Lloyd’s of London. Set for Life Insurance designs portable non-cancellable own-occupation policies through Principal, The Standard, Guardian, MassMutual, Ameritas, and Lloyd’s of London. Executive income protection coverage protects your base salary, bonus income, and incentive compensation through retirement. See this page for business owners who need to protect both their personal income and their business overhead expenses.

How Executive Disability Insurance Works

Executive disability insurance is a non-cancellable own-occupation individual policy that pays a monthly benefit to a corporate executive who can no longer perform the substantial and material duties of their occupation.

Set for Life Insurance places policies for executives earning $250,000 and above through Principal, The Standard, Guardian, MassMutual, Ameritas, and Lloyd’s of London. Single-carrier benefits issue up to $35,000 per month at top occupational classes, with Lloyd’s of London stacking layer available for executives whose insurable income exceeds the single-carrier ceiling.

| Provision | How It Applies to an Executive Disability Policy |

|---|---|

| MoExecutive disability insurance is a non-cancellable own-occupation individual policy that pays a monthly benefit to a corporate executive who can no longer perform the substantial and material duties of their occupation.nthly Benefit Amount | Individual disability benefits are non-taxable when the executive pays premiums with after-tax dollars, under IRC Section 104(a)(3). Employer-paid premiums produce benefits that are taxable as ordinary income at the time of claim. The distinction is material at executive income levels. A $15,000 monthly benefit paid tax-free and a $15,000 monthly benefit taxed at a combined federal and state marginal rate of 45 percent are not equivalent. Most carriers will insure 60 to 70 percent of pre-tax income, coordinated across all individual and group disability coverage currently in force. |

Get Your Customized Executive Quote

Compare Executive Disability Quotes Side-by-Side

"*" indicates required fields

She made updating my files with each life event stress-free. I watched colleagues struggle to communicate with insurance companies, but not me. One email to Jamie and everything is taken care of. My family is protected and done so with ease, all thanks to Jamie. I highly recommend Set For Life!!!

Carriers and Policy Options for High-Income Executives

What Is Executive Disability Insurance?

Executive disability insurance is individual income protection coverage purchased separately from employer group long-term disability. The policy is owned by the executive, follows the executive through employer changes and relocations, and pays a non-cancellable monthly benefit during a qualifying disability. Issue limits at top occupational classes reach $35,000 per month at Principal and The Standard, with Lloyd’s of London participation available for executives whose insurable income exceeds the single-carrier ceiling.

| Provision | How It Applies to an Executive Disability Policy |

|---|---|

| Non-Cancelable and Guaranteed Renewable | A non-cancelable, guaranteed-renewable policy is the most protective contractual structure available on individual disability insurance. Premiums are locked at the level set on the issue date and cannot be increased for the life of the policy. The carrier cannot modify the contract, add exclusions, or change terms after issue, even if the insured’s health status, occupation, or compensation changes. The executive who buys at 38 keeps the same premium, the same definition of disability, and the same riders at 58, regardless of subsequent promotions, weight gain, blood pressure changes, or diagnosis history. Most individual policies from Ameritas, Guardian, MassMutual, Principal, and The Standard include this provision as part of the base contract. A guaranteed-renewable-only policy gives the carrier the right to increase premiums on an entire class of policyholders, a materially weaker protection over a 20- or 30-year policy life. |

Own-Occupation vs. Residual Disability Insurance

Own-occupation coverage pays full benefits when the executive cannot perform the substantial and material duties of their specific role, even if working in another field. Residual disability coverage pays a partial benefit when the executive can still work but has lost a defined percentage of monthly earnings. Most executive policies include both. Set for Life Insurance configures the two definitions together so the policy covers total disability, partial disability, and the gray zones in between.

Future Increase Option Riders

Future increase option riders allow executives to raise the monthly benefit later without new medical underwriting. Principal’s MY Benefit rider permits income-based increases in years one through three and life-event triggered increases through age 50 or 20 years. The Standard’s Automatic Increase Benefit raises the benefit 4 percent each year for six years, and the Benefit Increase Rider allows medical-free purchases every three years through age 50. The riders matter most for executives whose income is expected to grow significantly after policy issue.

Where to Start

| If you… | The right next step is… |

|---|---|

| Earn over $300,000 with employer-paid group long-term disability | Layer individual coverage on top of the group cap |

| Have a CPAP, an SSRI prescription, or a chiropractor visit in your medical record | Request a quote and you will receive a link to schedule an appointment with a broker. |

| Plan to leave the United States for more than six months | Review the foreign residence terms before the policy issues |

| Work at an employer with three or more colleagues interested in coverage | Ask about Multi-Life and Guaranteed Standard Issue discounts |

| Just received a promotion, a raise, or a new equity grant | Apply now to lock the rate at your current age and current occupation class |

High Income Disability Insurance for Executives Above the Group Cap

Group Long-Term Disability Benefit Caps

Employer-provided group long-term disability insurance typically caps monthly benefits at $10,000 to $15,000. Once an executive’s income exceeds $300,000, that cap covers a smaller and smaller share of total compensation.

Group plans also exclude bonuses, incentive pay, sales commissions, and equity compensation. For senior leaders with total annual compensation above $300,000, group coverage alone can replace less than half of actual income.

Employer-paid group benefits are also taxable as ordinary income at the time of claim. On a $20,000 monthly benefit at a combined federal and state marginal rate of 45 percent, the tax difference between an employer-paid policy and an executive-paid policy is $9,000 per month.

Supplemental individual policies from Principal, The Standard, Guardian, MassMutual, Ameritas, and Lloyd’s of London are portable and pay benefits tax-free when the executive pays the premium. This supplemental disability insurance for executives structure works alongside employer coverage to raise monthly benefits above group plan caps.

The full carrier-by-carrier residual disability comparison, covering income loss thresholds, benefit formulas, independent triggers, benefit periods, and recovery provisions across Ameritas, Guardian, Lloyd’s, MassMutual, Principal, and The Standard, appears in the table below.

| Ameritas Life Insurance Corp. 4501NC · Enhanced Residual Rider (AERES) |

Guardian Berkshire Life Insurance Co. of America ICC16 18ID · Provider Choice + Enhanced Partial Rider |

Lloyd’s Petersen International Underwriters PDI111521 · Optional Residual Rider |

Mass Mutual Massachusetts Mutual Life Insurance Co. ICC15-XLIS-RC · Extended Partial Disability (EPR) |

Principal Principal Life Insurance Company ICC22-800-IDI · Income Protector |

The Standard Standard Insurance Company B180(7/17) · Platinum Advantage + Residual Riders |

|

|---|---|---|---|---|---|---|

| 1 · Income Loss Threshold That Triggers Residual Benefits | ||||||

| Minimum income loss required % of prior earnings that must be lost before residual benefits begin |

15% loss of monthly earnings (Specimen) One of the lowest thresholds available. Rider text states: loss must be “at least 15% of your prior monthly earnings” due to sickness or injury. |

Loss of Income due to disability (Specimen) Guardian’s Enhanced Partial rider defines “Loss of Income” as the difference between Prior Income and Current Income attributable solely to the Injury or Sickness. No explicit percentage floor in the base rider, benefit scales proportionally with income loss. Must be Gainfully Employed. |

Optional rider, threshold per rider terms (Specimen) Base Lloyd’s specimen (PDI111521) notes “Residual Disability is an optional benefit that only applies if the rider was purchased.” Rider text not included in this specimen. Typical Lloyd’s/PIU residual riders require income loss and inability to perform all material duties. |

20 to 80% loss of Predisability Earnings (Standard) EPR benefit is payable when Monthly Earnings fall to 20% to 80% of Predisability Earnings. Below 20% earnings remaining triggers full benefit. Above 80% earnings remaining, no EPR benefit is paid. |

Loss of Earnings from own occupation (Specimen) Principal’s Residual Disability Benefit Rider requires a loss of Earnings due to Disability. The specimen confirms “Earnings” excludes unearned income. No explicit minimum percentage floor, benefit scales pro-rata with the earnings loss ratio. |

20% loss of Predisability Earnings (Enhanced); 15 to 20% for Short-Term version (Specimen) Specimen lists Basic, Enhanced, and Short-Term Residual riders. Enhanced Residual: benefit payable when Monthly Earnings are 20% to 80% of Predisability Earnings. |

| 2 · Monthly Benefit Calculation Formula | ||||||

| Residual benefit formula How the monthly residual check is calculated |

Residual Monthly Benefit = (Loss of Monthly Earnings / Prior Monthly Earnings) x Base Monthly Benefit (Specimen) First 6 months minimum: The greater of (a) 50% of base monthly benefit OR (b) the formula result. 75%+ loss rule: If loss exceeds 75% of prior monthly earnings, treated as 100% loss and full base benefit is paid. Prior earnings: Average of highest 12-month or 24-month period before disability, indexed annually for CPI-U after year 1. |

Partial Disability Benefit = (Loss of Income / Prior Income) x Monthly Benefit (Specimen) Prior Income: Average monthly income for either (a) last 24 calendar months, or (b) the two calendar years with highest earnings in the three years before disability, whichever is greater. Current Income: All income for services during disability, excluding pre-disability earned-but-not-yet-received income. Full benefit floor: If loss of income is 100% or more of Prior Income, full monthly benefit is paid. |

Proportional formula, rider required (Specimen) Rider language not included in this specimen. Lloyd’s/PIU residual riders typically use a proportional income-loss formula: (income loss / pre-disability income) x base benefit. Confirm with current rider filing. |

EPR Benefit = [(Predisability Earnings – Monthly Earnings) / Predisability Earnings] x Monthly Benefit (Standard) Full benefit if earnings are less than 20% of predisability earnings. No benefit if earnings are greater than 80% of predisability earnings. Prior earnings: Average of the 24 months before disability began. |

Residual Benefit = (Loss of Earnings / Prior Earnings) x Maximum Monthly Benefit (Standard) Prior Earnings: Average monthly Earnings for the 12 months before disability. Current Earnings: Earnings during the disability period, excludes passive/unearned income. Minimum benefit: Typically 50% of base benefit for first 6 months. |

Residual Benefit = [(Predisability Earnings – Monthly Earnings) / Predisability Earnings] x Basic Monthly Benefit (Standard) Full benefit trigger: If Monthly Earnings are less than 20% of Predisability Earnings, full Basic Monthly Benefit is paid. Basic Residual Rider: Flat 50% of base benefit when qualifying criteria met. Enhanced Residual Rider: Proportional formula above; includes Recovery Benefit. |

| 3 · Prior Total Disability Requirement, Can Residual Trigger Independently? | ||||||

| Independent trigger Does residual require a prior period of total disability, or can it trigger on its own? |

Fully independent, no prior total disability required (Specimen) Ameritas AERES rider states benefits begin the later of: (1) the day after the end of the Elimination Period, OR (2) the day following a period of total disability for which benefits have been paid. Either path is valid. Days of both total and residual disability satisfy the elimination period. |

Fully independent, no prior total disability required (Specimen) Guardian’s Enhanced Partial Disability Benefit Rider uses its own Elimination/Accumulation Period. The insured must satisfy the Accumulation Period but does not need to first be Totally Disabled. Residual days count toward satisfying the Elimination Period. |

Rider-dependent, verify current rider (Specimen) Lloyd’s specimen confirms residual is an optional rider. The base policy elimination period can be satisfied by successive periods of Total Disability or Residual Disability, but rider must be reviewed for independence trigger language. |

Fully independent, no prior total disability required (Standard) MassMutual’s EPR rider allows residual disability claims to trigger directly after the elimination period without a prior total disability period. Both total and partial disability days satisfy the elimination period. |

Fully independent, no prior total disability required (Standard) Principal’s residual/partial disability rider triggers after the elimination period regardless of whether any total disability period occurred. The elimination period can be met by residual disability days alone. |

Fully independent, no prior total disability required (Standard) Standard’s Enhanced Residual Disability Benefit Rider triggers after the Benefit Waiting Period is satisfied, independent of any total disability. Days of Disability during the Benefit Waiting Period need not be consecutive. |

| 4 · Benefit Period for Residual Disability | ||||||

| Residual benefit period Maximum duration for which residual benefits can be paid |

Remaining unused portion of the Total Disability Maximum Benefit Period (Specimen) The Residual Maximum Benefit Period equals the total unused portion of the maximum benefit period for total disability shown on the schedule. Combined total and residual payments cannot exceed this period. Typically to Age 65/67 when selected. |

Same Benefit Period as Total Disability, to Age 65, 67, or 70 (Specimen) Benefit Periods of To Age 70/67/65 or 10/5/2 Years are available. The Enhanced Partial rider benefit period matches the policy benefit period. To Age 70 option available for physicians, which is distinctive among carriers. |

Per Schedule of Benefits / rider terms (Specimen) The residual rider benefit period is set at time of issue and shown on the Schedule of Benefits (Section 1-D). Confirm with current rider. |

To Age 65 (base); Extended to Age 65 via Maximum Benefit Period Endorsement (Specimen) Specimen shows coverage end date for Extended Partial Disability corresponding to the policy’s non-cancellable period to age 65. A separate Maximum Benefit Period Endorsement is available with its own premium schedule. |

Same as base policy Maximum Benefit Period, 2 years, 5 years, To Age 65/67/70 (Specimen) Options include To Age 65, 67, and 70. Residual benefits run within this same period. To Age 70 available depending on occupation class. |

Same as base policy Maximum Benefit Period, to Age 67 in this specimen (Specimen) Maximum Benefit Period schedule applies (e.g., if disability begins at 62: 60 months; at 63: 48 months). Enhanced Residual Disability Benefit Rider matches base benefit period. |

| 5 · Recovery Benefit Provisions | ||||||

| Recovery benefit Protections after returning to work, continued payments if income remains depressed |

Explicit Recovery Benefit provision (Specimen) Triggers after a disability benefit period ends if the insured has returned to work, is performing material duties 80% or more of prior time, and still has 15% or more loss of monthly earnings demonstrably caused by the prior disability. Duration: Continues up to the residual maximum benefit period. |

Recovery Benefit, income-loss based, ongoing (Specimen) Benefits continue post-recovery as long as Loss of Income persists due to the disability. Because Guardian uses an income-loss formula, benefits naturally continue as long as Current Income remains below Prior Income due to the disabling condition. Prior Income protection: Uses the best 24-month or best-2-of-3-years average. |

Recovery benefit per rider, verify current rider (Specimen) Lloyd’s base specimen does not contain recovery benefit language. Standard Lloyd’s/PIU residual riders may include recovery provisions, but this must be confirmed against the current executed rider. |

Recovery Benefit included in EPR rider (Standard) After returning to full-time work following a disability for which EPR benefits were paid, if Monthly Earnings remain below Predisability Earnings due to the disability, a proportional recovery benefit continues. Duration: up to the remaining Maximum Benefit Period. |

Recovery Benefit, proportional, ongoing post-return (Standard) Provides recovery benefits when an insured has returned to Full Time Work but Earnings remain below prior levels due to the disability. Benefit calculated using the same proportional formula. |

Recovery Benefit included, Enhanced Residual Rider only (Specimen) The Basic Residual Rider does not include the Recovery Benefit, the Enhanced version is required. The base policy confirms premiums are waived while Recovery Benefits are payable. Short-Term Residual Rider: does not include recovery benefit. |

Source: Specimen policy language cited from each carrier’s residual disability rider, current as of each carrier’s most recently published filing. Set for Life Insurance verifies current terms at the time of quoting. Each of the five sections above functions as its own single-row comparison, so no additional fancy summary row was added.

Executive Disability Income Insurance and What Compensation Counts

Restricted Stock Units and Deferred Compensation Exclusions

Executive disability insurance benefits are calculated from earned compensation, which carriers define narrowly. Base salary counts at every major carrier.

Annual bonuses and sales commissions count once a documented two-year history exists, typically through tax returns or W-2s. The 401(k) and FSA contributions are add-backs at Principal.

Restricted stock units, stock options, deferred compensation, and other equity grants are typically excluded from the benefit calculation. Principal’s product guide states that earnings “do not include any form of unearned income such as dividends, rents, interest, capital gains, income received from any form of deferred compensation, retirement, pension plan, income from royalties, or disability benefits.”

The operative W-2 income figure is typically box 5, Medicare wages and tips, which captures vested restricted stock unit income at vest but not unvested grants or deferred compensation accruals. Executives with equity-heavy compensation should size the benefit to vested W-2 income rather than to total compensation.

The Standard does not address equity compensation in its income documentation table. MassMutual flags hedge fund carry and venture capital allocations for individual underwriter pre-approval rather than automatic inclusion or exclusion.

| Compensation Element | Principal | The Standard | MassMutual |

|---|---|---|---|

| Base salary | Included | Included | Included |

| Annual bonus | Included | Included with two years of tax-return documentation | Included with W-2 or paystub documentation |

| Sales commissions | Included | Included with two years of tax-return documentation | Included with W-2 documentation |

| 401(k) and FSA contributions | Add-back permitted | Not specified | Not specified |

| Stock options and RSUs | Explicitly excluded | Not addressed in income documentation table | Not addressed in source document |

| Deferred compensation | Explicitly excluded | Not addressed | Not addressed |

| Hedge fund carry and venture capital allocations | Not specifically flagged | Not addressed | Flagged for individual underwriter pre-approval |

Own Occupation Disability Insurance for Executives and Occupation Class Standing

Own-Occupation Period Coverage and Residual Disability Triggers

A corporate executive earning $250,000 or more in office-based managerial work typically qualifies for occupation class 5A or higher. MassMutual’s Executive Underwriting Program upgrades qualifying executives to class 5A/5, the top of its ten-tier ladder, when income exceeds $250,000, manual duties stay below 10 percent, sales activities stay below 20 percent, and tenure exceeds five years.

Principal classifies finance and portfolio management executives at class 5A or 6A+ when income exceeds $200,000 over the prior two years. The Standard places office-based managers and executives earning $100,000 or more each of the last two years at class 5A and applies a 20 percent Preferred Occupation Discount. Higher classes carry lower premiums for the same benefit.

The own-occupation period for executives determines how residual disability benefits trigger. At MassMutual, Principal, and The Standard, residual disability can trigger independently of any prior period of total disability. The carrier-by-carrier independent-trigger comparison appears in the residual disability table in the section above.

Occupational Classification Rules Carriers Apply

Occupational classification at every major carrier is based on duties actually performed, not job title. A job title alone is not sufficient to set the class; the carrier reviews the specific tasks the applicant performs day to day.

When an applicant holds multiple occupations, carriers apply the rule for the lower-risk occupation differently. Ameritas, Guardian, and Principal apply the lower occupational class to the entire policy. The Standard instead classifies based on whichever occupation carries the greatest risk.

Every carrier sets a 30-hour-per-week floor to qualify as full-time for classification purposes. Manual-duty limits determine access to the top tier: Guardian allows up to 10 percent manual duties at Class 5 and requires zero manual duties for Class 6, while MassMutual, Principal, and The Standard require office-only duties at their respective top tiers.

Top-tier income thresholds vary by carrier: roughly $75,000 or more at Ameritas and Guardian, up to $250,000 at MassMutual for the 5A/5 corporate executive tier, $200,000 or more at Principal for its 6A+ business-owner tier, and $150,000 or more at The Standard for top-tier classification, though this varies by occupation. Carriers also apply stable-business requirements, such as Guardian’s five-years-in-business standard with at least five employees in classes four through six, before granting top-tier classification.

Class-upgrade programs let an executive move to a better tier as income and tenure grow. Ameritas offers a 5 percent premium credit for preferred occupations in classes 6A through 4A, and Guardian’s Move-Up Option applies named criteria across a lettered list. MassMutual and Principal both run Business Owner and Executive Upgrade programs, and Principal stacks discounts up to 35 percent for qualifying multi-life GSI groups.

The carrier-by-carrier occupation class underwriting principles comparison, covering qualification thresholds, duty-based classification rules, multi-occupation rules, and premium discounts, appears in the table below.

| Ameritas Life Insurance Corp. Field Underwriting Guide |

Guardian Berkshire Life Insurance Co. of America Provider Choice · IDI Field Underwriting Guide |

Mass Mutual Massachusetts Mutual Life Insurance Co. Radius Choice · Underwriting Guide |

Principal Principal Life Insurance Company Income Protector · Disability Product Guide |

The Standard Standard Insurance Company Platinum Advantage · Product Guide |

|

|---|---|---|---|---|---|

| Top-tier annual income required to qualify | ~$75,000+ | ~$75,000+ | ~$250,000+ | ~$200,000+ | ~$150,000+ |

| Classification based on duties, not job title | Yes, explicitly stated | Yes, explicitly stated (Section 7, rule 5) | Yes, “A job title alone is not sufficient” | Yes, explicitly stated (Section 16) | Yes, “Specify the duties of the applicant’s occupation, not just the title” |

| Rule for applicants with multiple occupations | Lower occupational class prevails | Lower occupational class prevails | Lower class prevails and applies to the entire contract | Lower class prevails | Occupation with the greatest risk determines the class |

| Minimum hours per week to qualify (full-time threshold) | 30 hours | 30 hours | 30 hours | 30 hours | 30 hours |

| Manual-duty cap for top-tier class | No manual duties | 0% manual (Class 6); ≤10% manual (Class 5) | No manual duties, office only | Office-only for the 6A+ tier | Office-only for the 5A tier |

| Income threshold for top-tier classification | $75,000+ (5A) / $100,000+ (6A consultant tier) | $75,000+ (Class 6) / $60,000+ (Class 5) | Up to $250,000+ for 5A/5 corporate executive tier | $200,000+ for the 6A+ business-owner tier | $150,000+ for top-tier insurance producers; varies by occupation |

| Stable-business requirement for top-tier classification | 5 years in business, 10+ employees | 5 years in business, 10+ employees with at least 5 in classes 4 to 6 | 5 years in business with employee and ownership tests | Varies by occupation | 5 years continuous experience (varies by occupation) |

| Class upgrade or “Move-Up” program | “Preferred Occupations” 5% premium credit for 6A to 4A | “Move-Up Option” with named criteria A through P | Business Owner Upgrade and Executive Upgrade Programs | Business Owner Program with three income tiers | Business Owner Upgrade and Earned Income Enhancer |

| Premium discounts available based on class | 5% credit for preferred occupations (6A to 4A) | 10% Preferred Occupation Discount (POD) on eligible specialties | Modifier-based pricing tiers (Radius Choice) | Stackable discounts up to 35% (multi-life GSI), 20% (multi-life), 10% (association) | Multi-life and business owner discounts; gender-neutral options |

Source: Field underwriting guides published by each carrier. Thresholds and discount percentages are subject to change at carrier discretion and may vary by state. Set for Life Insurance verifies current values at the time of quoting.

Occupation Class Structure Across Carriers

Set for Life Insurance places executive disability coverage with Principal Financial Group, The Standard, Guardian, Berkshire Life Insurance Co. of America, MassMutual, Ameritas, and Petersen International Underwriters at Lloyd’s of London. Each carrier offers individual non-cancellable own-occupation disability insurance for high-income executives, with policy issue limits typically capping at $35,000 per month at the top occupational classes.

Lloyd’s of London participation is available as a stacking layer above the carrier maximum for executives whose insurable income exceeds the single-carrier ceiling. Principal additionally offers DI Retirement Security as a separate policy that protects retirement contributions during a disability claim.

The broker recommends the carrier and product combination based on occupational class, age, health profile, compensation structure, and the executive’s planning objectives. The occupation class structure comparison below shows where an executive’s own occupation class 5A or 6A stands on each carrier’s non-medical ladder.

| Ameritas Life Insurance Corp. Field Underwriting Guide |

Guardian Berkshire Life Insurance Co. of America Provider Choice · IDI Field Underwriting Guide |

Mass Mutual Massachusetts Mutual Life Insurance Co. Radius Choice · Underwriting Guide |

Principal Principal Life Insurance Company Income Protector · Disability Product Guide |

The Standard Standard Insurance Company Platinum Advantage · Product Guide |

|

|---|---|---|---|---|---|

| Top non-medical class, the executive occupation ceiling | 6A | Class 6 | 5A/5 (with Radius Choice modifier) | 6A+ | 5A |

| Total distinct insurable classes | ~13 | ~14 | ~17 | ~22 | ~12 |

| Lowest insurable non-medical class | B | Class 2 | A | 1A | B |

| Sub-tier or plus modifiers between main non-medical classes | None | None | Yes, Radius Choice modifiers within the executive ladder (5A/5, 5A/3, 4A/3, 4A/2, 4A/1) | Yes, extensive plus modifiers within the executive ladder (6A+, 2A+) | Limited, no intermediate designation within the non-medical executive ladder |

Source: Field underwriting guides published by each carrier. Class names and product identifiers are taken from the most recently published producer-facing guides held by Set for Life Insurance. Class assignments are subject to underwriter review at the time of application. Table scoped to non-medical occupation classes relevant to executive applicants; medical- and dental-specific class tracks are not shown here.

Disability Insurance for Highly Compensated Employees and Executive Groups

Renewal Option and Executive Benefit Period Length

Standard benefit periods for executive disability insurance include 2 years, 5 years, 10 years, to age 65, and to age 67. No major carrier issues a lifetime benefit period to executives.

Late-life claims carry graded payout schedules. On a Principal to-age-65 policy, a disability after age 61 pays 48 months rather than the full remaining period. On a Standard to-age-67 policy, a disability at age 65 pays 36 months.

The policy remains non-cancellable and guaranteed renewable to the termination date, meaning the insurer cannot raise premium or change terms during that period. This non-cancellable contract structure is what makes the benefit period a fixed commitment rather than a renewable estimate. The Standard offers a Renewal Option past the termination date for executives working 30 or more hours per week.

The full benefit-period comparison across Ameritas, Guardian, Lloyd’s, MassMutual, Principal, and The Standard, including each carrier’s residual benefit period rules, appears in the table above.

Working Abroad and the Foreign Residence Clause

Principal and The Standard both cap disability benefits at 12 months of payment while the insured is living outside the United States and Canada. Principal requires residence in the U.S. or Canada for at least six consecutive months in each calendar year for benefits to continue beyond 12 months.

The Standard’s foreign residence clause is required by California, Florida, Montana, New York, North Dakota, South Dakota, and Wyoming. Executives planning a multi-year international assignment should review the residence terms with the broker before the assignment begins.

Pre-issue travel disclosure is the only window in which destination affects coverage. Once a policy is in force, short-term travel does not affect benefits.

Multi-Life Eligibility for Executive Groups

Executives with certain health histories may be eligible for Guaranteed Standard Issue disability insurance, which does not require medical underwriting. GSI programs available through Set for Life Insurance offer fixed benefits of up to $15,000 per month and approval within five business days.

These GSI arrangements may be set up through the employer when three or more employees apply for coverage together, and the resulting policies are referred to as Multi-Life policies. Guardian, Principal Financial Group, MassMutual, Ameritas, and The Standard all provide these programs for executives affiliated with approved organizations or professional associations.

Principal’s Employer Multi-Life program offers discounts up to 35 percent stacked with Guaranteed Standard Issue underwriting, requires home-office approval plus an employee census, applies to occupation classes 3A and higher, and accepts a minimum of five employer-paid lives. The Standard’s Employer-Based Multi-Life Discount is 10 percent on Platinum Advantage for three or more lives from the same employer within a six-month window.

Policies issued under a Multi-Life program are individually owned and remain portable when the executive leaves the company. The arrangement reduces premium, simplifies underwriting through the Guaranteed Standard Issue mechanism, and makes coverage available to executives whose medical history might otherwise complicate individual issue.

Preferred Occupation Discount and Employer Multi-Life Savings

Discounts available to executives stack across multiple programs. The Standard offers a 20 percent Preferred Occupation Discount on Platinum Advantage for 5A executives in office-based managerial roles earning $100,000 or more each of the prior two years.

A 10 percent Employer-Based Multi-Life Discount applies when three or more executives from the same employer apply within six months. Additional 5 percent discounts apply for multi-product purchase, eApply usage, and GSI cross-sale.

Principal applies a Multi-Life Employer discount up to 20 percent layered with a GSI discount up to 35 percent for qualifying executive groups. Association memberships in groups such as the American Bar Association can add 10 to 15 percent discounts depending on carrier.