Disability Insurance for Medical Residents

Best Disability Insurance for Medical Residents

Disability Insurance for Residents

Resident Disability Insurance Quotes

Lock in coverage before you finish medical school. Discounted disability insurance for medical residents with special pricing during training. Set for Life Insurance offers guaranteed standard issue options at hospitals nationwide. Secure own-occupation protection without medical underwriting and protect your investment in medical training with GSI disability insurance for residents and fellows. Portable coverage throughout your career.

Get Your Customized Resident Quote

Compare Resident Disability Quotes Side-by-Side

"*" indicates required fields

She made updating my files with each life event stress-free. I watched colleagues struggle to communicate with insurance companies, but not me. One email to Jamie and everything is taken care of. My family is protected and done so with ease, all thanks to Jamie. I highly recommend Set For Life!!!

Disability Insurance for Doctors, Dentists, and Veterinarians

Disability Risk for Doctors in Medical Residency

Student Loans and Lost Income When a Resident Goes on Disability

Roughly 25 percent of physicians experience a disability lasting 90 days or longer during their careers. Medical residents enter that risk window carrying student loan debt that does not disappear if a disability strikes, while their highest-earning years as attending physicians still lie ahead.

Clinical training is physically demanding work. Long shifts, sustained physical exertion, and high-stress environments put residents at higher risk of disabling injury or illness than many other professionals face at the same career stage.

Set for Life Insurance’s Jamie Fleischner has worked with residents who developed conditions during training, including back injuries, cancer, and diabetes. Residents who secured medical resident disability insurance early kept their financial security and career options intact. Others who waited faced difficult choices about continuing their medical education.

A resident’s most valuable asset during training is future earning ability as a physician, built on years of education and debt that a disability does not erase. Disability insurance for medical residents protects that asset during medical residency, the vulnerable stretch when income is lowest but the investment in training is highest.

Group Disability Plan Versus Individual Disability Plan for Residents

When Your Residency Program Offers Coverage With No Health Questions

Guaranteed Standard Issue disability insurance is available at select hospitals through designated brokers, including Set for Life Insurance. GSI approval requires no medical underwriting, no physical examination, and no health questionnaire, which makes it valuable for a resident who already has a health condition on record, including Type 1 diabetes or a history of back surgery.

GSI benefit amounts typically run from $5,000 to $7,500 monthly during residency, with future increases available up to $15,000 monthly without any additional medical questions. Premiums under GSI may run slightly higher than a traditionally underwritten policy, a tradeoff for skipping medical underwriting entirely. True Own-Occupation protection applies from day one, meaning full specialty-specific coverage exists from the start rather than being phased in, and Medical Resident Benefits under a GSI policy remain portable through fellowship, employer changes, and geographic moves.

Professional association programs through medical organizations offer another path to residency coverage worth comparing against a GSI program. Residents whose training hospital does not offer a hospital-sponsored GSI program, or who want to compare GSI against an individually underwritten policy, can review eligibility and deadlines on the GSI program page.

Benefit Caps, Taxability, and Portability of Employer Coverage

A Group Disability Plan from a hospital provides basic protection with real limits. Most hospital group policies cap monthly benefits at $10,000 to $15,000 and require total disability under an any-occupation standard before benefits are paid, with no partial disability provision for a resident who can work reduced hours. Based on Set for Life Insurance’s 30-plus years of experience, roughly 80 percent of physicians supplement group coverage with an Individual Disability Plan.

An any-occupation definition means a physician could lose benefits if able to work in any job for which training or experience qualifies them, even at a fraction of a medical specialty’s salary. An own-occupation Individual Disability Plan pays full benefits if a resident cannot work in their medical specialty, even while remaining capable of other work, and many individual policies add a partial disability rider that pays a prorated benefit if the resident can work reduced hours. A surgeon with hand tremors would receive full benefits under an own-occupation policy while still able to teach, a claim that could be denied under a group any-occupation standard.

Group coverage does not follow a physician who changes employers, and group benefits may be taxable when the employer pays the premium. A hospital-provided $10,000 monthly benefit, if employer-paid, may net only $5,000 to $6,000 after taxes depending on tax bracket, even while the physician remains on disability and unable to work. Few physicians stay with the same employer for an entire career, and group policies rarely cover locum, gig, or self-employed work, a gap that widens exactly when a resident’s career becomes more mobile.

Residency Disability Insurance Premiums, Discounts, and Coverage Increases

Graded Premiums and Resident Discounts During Medical Training

A starter disability policy for a resident can cost around $50 monthly using a graded premium structure, with resident discounts of 10 to 15 percent available from major carriers including Guardian, MassMutual, Principal Financial Group, The Standard, and Ameritas. Set for Life Insurance recommends residents start with a minimum-sized policy providing $2,500 in monthly benefits, since graded premiums increase gradually each year rather than starting at full price. Rates vary based on gender, medical specialty, age, and the benefit amount chosen.

The strategy is to start small and expand later. A resident begins with a minimum-sized policy, then raises coverage after residency, often from $2,500 to $10,000 per month or more, as income grows, without new medical underwriting as long as the resident meets the income requirements tied to the increase.

Less expensive coverage during residency does not mean inferior coverage. These policies still carry true own-occupation definitions. The lower cost comes from starting with a smaller benefit amount and applying resident-specific discounts, not from weaker policy terms.

Getting Disability Insurance Early Locks In Premiums and Insurability

Getting disability insurance early in training, while young and healthy, is the single biggest lever a resident has over price and terms. Carriers review an applicant’s medical history for the previous 10 years at the time of application, and residents are unlikely to become healthier as time passes.

Once a carrier approves a policy, no further medical questions apply for the life of that coverage, even if health changes later or the resident later goes on disability. This locks in insurability at the healthiest point in a resident’s career and secures better pricing than waiting would allow.

Applying before engaging in higher-risk activities, such as skiing, climbing, or riding a motorcycle, also matters. Coverage secured before those activities begin avoids exclusions tied to the activity. Many residents apply specifically before ski season or adventure travel for this reason.

Future Increase Options That Raise Benefits As Income Grows

Future increase options and guaranteed insurability riders let a resident raise coverage after training without new medical exams or health questions, based on proof of the new, higher salary. Income verification typically requires tax returns or an employment contract, not a health evaluation.

GSI policies allow increases up to $15,000 monthly without additional medical questions. Non-GSI policies allow larger increases, up to $25,000 monthly, though they were medically underwritten at the outset. A resident earning $70,000 to $80,000 in training can move to attending-level income of $200,000 to $400,000 or more and increase coverage to match, without a new health review at either step.

Carrier Options for Resident Disability Insurance

True Own-Occupation and Specialty Specific Definitions by Carrier

Resident physician disability coverage pays benefits if a resident cannot perform the substantial and material duties of their medical specialty due to sickness or injury, even if they remain capable of other work, as long as the policy carries a true own-occupation, specialty specific definition. Any-occupation coverage requires total incapacity from any occupation the resident is reasonably suited for by education, training, or experience, a materially weaker standard for a physician.

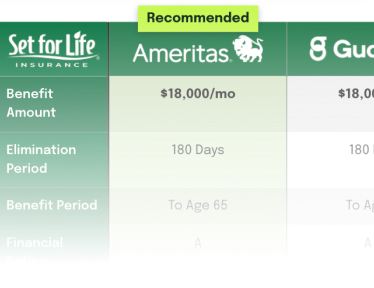

Ameritas confirms true specialty own-occupation for physicians and dentists, with a 15 percent income loss threshold among the lowest tested, plus CPI-U indexing of prior earnings during a claim. Guardian’s Berkshire Life policy adds a Surgical Procedure Enhancement and Hands-on Patient Care Enhancement, triggering total disability solely from the loss of surgical or hands-on capacity if that work generates more than half of income, with a benefit period available to age 70.

MassMutual is a participating policy eligible for dividends and includes a RetireGuard rider that protects retirement contributions during disability, a feature unique to MassMutual. Principal Financial Group confirms specialty own-occupation for a single professionally recognized specialty and offers an Annual Increase Rider adding an automatic 3 percent benefit increase at no added cost, plus a pandemic suspension provision. The Standard confirms specialty own-occupation recognized by ABMS, AOABOS, or ADA standards, structures its residual benefit in three tiers, and adds a Family Care Benefit that pays if a policyholder reduces hours to care for a seriously ill family member.

Guardian, MassMutual, Principal, Ameritas, and The Standard Compared

Guardian offers pure own-occupation definitions with added surgical specialty language.

MassMutual carries strong financial ratings and pays dividends yearly. Principal Financial Group offers attractive pricing for younger physicians with adjustable policies.

Ameritas provides solid coverage with favorable terms for residents. The Standard includes a Compassionate Care rider that pays benefits if a policyholder needs to care for a family member.

Premium structures vary by choice as much as by carrier. Level premiums stay the same throughout a career, while graded premiums start lower and increase annually during residency, then can convert to level rates later. Resident-specific discounts of 10 to 15 percent often continue into attending years regardless of which structure a resident chooses.

Comparison factors worth checking include the strength of the own-occupation definition, the future increase option limit, whether a GSI program is available through the resident’s hospital, and how the premium structure fits expected income growth. An independent broker like Set for Life Insurance compares all five carriers side by side and aligns policy terms with a resident’s career trajectory.

| Data Point | Ameritas Life Insurance Corp. 4501NC, Enhanced Residual Rider (AERES) |

Guardian Berkshire Life Insurance Co. of America ICC16 18ID, Provider Choice + Enhanced Partial Rider |

Mass Mutual Massachusetts Mutual Life Insurance Co. ICC15-XLIS-RC, Extended Partial Disability (EPR) |

Principal Principal Life Insurance Company ICC22-800-IDI, Income Protector |

The Standard Standard Insurance Company B180(7/17), Platinum Advantage + Residual Riders |

|---|---|---|---|---|---|

| 1. Income Loss Threshold That Triggers Residual Benefits | |||||

| Minimum income loss required % of prior earnings that must be lost before residual benefits begin |

15% loss of monthly earnings (Specimen) One of the lowest thresholds available. Rider text states: loss must be “at least 15% of your prior monthly earnings” due to sickness or injury. |

Loss of Income due to disability (Specimen) Guardian’s Enhanced Partial rider defines “Loss of Income” as the difference between Prior Income and Current Income attributable solely to the Injury or Sickness. No explicit percentage floor in the base rider, benefit scales proportionally with income loss. Must be Gainfully Employed. |

20–80% loss of Predisability Earnings (Standard) EPR benefit is payable when Monthly Earnings fall to 20%–80% of Predisability Earnings. Below 20% earnings remaining triggers full benefit. Above 80% earnings remaining, no EPR benefit is paid. |

Loss of Earnings from own occupation (Specimen) Principal’s Residual Disability Benefit Rider requires a loss of Earnings due to Disability. The specimen confirms “Earnings” excludes unearned income. No explicit minimum percentage floor, benefit scales pro-rata with the earnings loss ratio. |

20% loss of Predisability Earnings (Enhanced); 15–20% for Short-Term version (Specimen) Specimen lists Basic, Enhanced, and Short-Term Residual riders. Enhanced Residual: benefit payable when Monthly Earnings are 20%–80% of Predisability Earnings. |

| 2. Monthly Benefit Calculation Formula | |||||

| Residual benefit formula How the monthly residual check is calculated |

Residual Monthly Benefit = (Loss of Monthly Earnings / Prior Monthly Earnings) x Base Monthly Benefit (Specimen) First 6 months minimum: The greater of (a) 50% of base monthly benefit OR (b) the formula result. 75%+ loss rule: If loss exceeds 75% of prior monthly earnings, treated as 100% loss and full base benefit is paid. Prior earnings: Average of highest 12-month or 24-month period before disability, indexed annually for CPI-U after year 1. |

Partial Disability Benefit = (Loss of Income / Prior Income) x Monthly Benefit (Specimen) Prior Income: Average monthly income for either (a) last 24 calendar months, or (b) the two calendar years with highest earnings in the three years before disability, whichever is greater. Current Income: All income for services during disability, excluding pre-disability earned-but-not-yet-received income. Full benefit floor: If loss of income is 100% or more of Prior Income, full monthly benefit is paid. |

EPR Benefit = [(Predisability Earnings – Monthly Earnings) / Predisability Earnings] x Monthly Benefit (Standard) Full benefit if earnings are less than 20% of predisability earnings. No benefit if earnings are greater than 80% of predisability earnings. Prior earnings: Average of the 24 months before disability began. |

Residual Benefit = (Loss of Earnings / Prior Earnings) x Maximum Monthly Benefit (Standard) Prior Earnings: Average monthly Earnings for the 12 months before disability. Current Earnings: Earnings during the disability period, excludes passive/unearned income. Minimum benefit: Typically 50% of base benefit for first 6 months. |

Residual Benefit = [(Predisability Earnings – Monthly Earnings) / Predisability Earnings] x Basic Monthly Benefit (Standard) Full benefit trigger: If Monthly Earnings are less than 20% of Predisability Earnings, full Basic Monthly Benefit is paid. Basic Residual Rider: Flat 50% of base benefit when qualifying criteria met. Enhanced Residual Rider: Proportional formula above; includes Recovery Benefit. |

| 3. Prior Total Disability Requirement, Can Residual Trigger Independently? | |||||

| Independent trigger Does residual require a prior period of total disability, or can it trigger on its own? |

Fully independent, no prior total disability required (Specimen) Ameritas AERES rider states benefits begin the later of: (1) the day after the end of the Elimination Period, OR (2) the day following a period of total disability for which benefits have been paid. Either path is valid. Days of both total and residual disability satisfy the elimination period. |

Fully independent, no prior total disability required (Specimen) Guardian’s Enhanced Partial Disability Benefit Rider uses its own Elimination/Accumulation Period. The insured must satisfy the Accumulation Period but does not need to first be Totally Disabled. Residual days count toward satisfying the Elimination Period. |

Fully independent, no prior total disability required (Standard) MassMutual’s EPR rider allows residual disability claims to trigger directly after the elimination period without a prior total disability period. Both total and partial disability days satisfy the elimination period. |

Fully independent, no prior total disability required (Standard) Principal’s residual/partial disability rider triggers after the elimination period regardless of whether any total disability period occurred. The elimination period can be met by residual disability days alone. |

Fully independent, no prior total disability required (Standard) Standard’s Enhanced Residual Disability Benefit Rider triggers after the Benefit Waiting Period is satisfied, independent of any total disability. Days of Disability during the Benefit Waiting Period need not be consecutive. |

| 4. Benefit Period for Residual Disability | |||||

| Residual benefit period Maximum duration for which residual benefits can be paid |

Remaining unused portion of the Total Disability Maximum Benefit Period (Specimen) The Residual Maximum Benefit Period equals the total unused portion of the maximum benefit period for total disability shown on the schedule. Combined total and residual payments cannot exceed this period. Typically to Age 65/67 when selected. |

Same Benefit Period as Total Disability, to Age 65, 67, or 70 (Specimen) Benefit Periods of To Age 70/67/65 or 10/5/2 Years are available. The Enhanced Partial rider benefit period matches the policy benefit period. To Age 70 option available for physicians, distinctive among carriers. |

To Age 65 (base); Extended to Age 65 via Maximum Benefit Period Endorsement (Specimen) Specimen shows coverage end date for Extended Partial Disability corresponding to the policy’s non-cancellable period to age 65. A separate Maximum Benefit Period Endorsement is available with its own premium schedule. |

Same as base policy Maximum Benefit Period, 2 years, 5 years, To Age 65/67/70 (Specimen) Options include To Age 65, 67, and 70. Residual benefits run within this same period. To Age 70 available depending on occupation class. |

Same as base policy Maximum Benefit Period, to Age 67 in this specimen (Specimen) Maximum Benefit Period schedule applies (e.g., if disability begins at 62: 60 months; at 63: 48 months). Enhanced Residual Disability Benefit Rider matches base benefit period. |

| 5. Recovery Benefit Provisions | |||||

| Recovery benefit Protections after returning to work, continued payments if income remains depressed |

Explicit Recovery Benefit provision (Specimen) Triggers after a disability benefit period ends if the insured has returned to work, is performing material duties 80% or more of prior time, and still has 15% or more loss of monthly earnings demonstrably caused by the prior disability. Duration: Continues up to the residual maximum benefit period. |

Recovery Benefit, income-loss based, ongoing (Specimen) Benefits continue post-recovery as long as Loss of Income persists due to the disability. Because Guardian uses an income-loss formula, benefits naturally continue as long as Current Income remains below Prior Income due to the disabling condition. Prior Income protection: Uses the best 24-month or best-2-of-3-years average. |

Recovery Benefit included in EPR rider (Standard) After returning to full-time work following a disability for which EPR benefits were paid, if Monthly Earnings remain below Predisability Earnings due to the disability, a proportional recovery benefit continues. Duration: up to the remaining Maximum Benefit Period. |

Recovery Benefit, proportional, ongoing post-return (Standard) Provides recovery benefits when an insured has returned to Full Time Work but Earnings remain below prior levels due to the disability. Benefit calculated using the same proportional formula. |

Recovery Benefit included, Enhanced Residual Rider only (Specimen) The Basic Residual Rider does not include the Recovery Benefit, the Enhanced version is required. The base policy confirms premiums are waived while Recovery Benefits are payable. Short-Term Residual Rider: does not include recovery benefit. |

| 6. Physician-Specific Nuances and Notable Provisions | |||||

| Key nuances for physicians Provisions especially relevant to medical specialists |

True specialty own-occupation for physicians/dentists (specimen confirmed) 15% income loss threshold is the lowest tested, ideal for physicians cutting back patient load CPI-U indexing of prior earnings during claim protects against inflation eroding residual benefit Accounting method choice (cash or accrual) accommodates both employed and practice-owner physicians |

Surgical Procedure Enhancement and Hands-on Patient Care Enhancement (confirmed in specimen): If more than 50% of income comes from surgical procedures or hands-on care, total disability is triggered solely by loss of that capacity To Age 70 benefit period available Income includes business profits from privately held entities Prior Income = best 24 months OR best 2-of-3 years |

Participating policy, eligible for dividends (not guaranteed) RetireGuard rider protects retirement contributions during disability, unique to MassMutual Own Occupation Rider available separately from the EPR, both can be elected simultaneously Short-Term Disability Benefits Rider (STR) included within the EPR structure |

Specialty own-occupation confirmed: “single professionally recognized specialty in medicine or dentistry” is deemed own occupation True Own Occupation add-on available at additional cost Annual Increase Rider (AIR): automatic 3% benefit increase, no additional cost, to earlier of 20 years or age 50 Pandemic suspension provision, unique feature allowing suspension during declared pandemic |

Specialty own-occupation confirmed: “single specialty recognized by ABMS, AOABOS, or ADA” is deemed own occupation Three-tier residual structure: Basic / Enhanced / Short-Term Family Care Benefit: pays if working reduced hours to care for a seriously ill family member, no total disability required Survivor Benefit: 3x basic monthly benefit paid to beneficiary if death occurs while benefits are payable Platinum Advantage specimen is for limited states (CT, DE, DC, FL, MT, ND, SD) |

Specimen policy forms cited above are Ameritas 4501NC with the Enhanced Residual Rider (AERES), Guardian’s Berkshire Life Insurance Co. of America ICC16 18ID with the Provider Choice and Enhanced Partial Rider, MassMutual’s ICC15-XLIS-RC with the Extended Partial Disability rider, Principal Life Insurance Company’s ICC22-800-IDI Income Protector, and The Standard’s B180(7/17) Platinum Advantage with Residual Riders. Confirm current policy language and rider availability with Set for Life Insurance before applying.

Portable Resident Physician Disability Coverage Through Fellowship and Practice

What Happens to Medical Resident Benefits at Graduation

Medical Resident Benefits continue at the end of residency and expand to match attending-level earnings, becoming the foundation for lifelong protection rather than a policy a resident replaces. Coverage expansion raises benefits from minimal resident levels to full attending income replacement and requires only income documentation, not a new health evaluation. Premiums adjust to reflect the higher benefit, and specialty adaptation keeps coverage aligned with the resident’s actual medical field as they move into practice.

Future increase options and guaranteed insurability riders let a resident move from $1,000 to $2,000 in monthly benefits during training up to substantial attending-level coverage, using proof of income such as pay stubs or an employment contract rather than a health review. GSI policies typically allow increases up to $15,000 monthly without medical questions, while traditional policies may allow higher limits depending on the carrier and the resident’s income.

A resident can also convert graded premiums to level rates at this stage and add policy riders when coverage increases, with additional increases sometimes available after fellowship.

Disability Income Insurance That Follows Doctors Into Fellowship and Practice

Disability income insurance, sometimes called income insurance, protects future income by locking in coverage and insurability during the earliest and healthiest stage of a medical career, then expanding to match higher earnings counted as income once a physician’s career advances. Coverage remains valid through fellowship training, geographic moves across state lines, and changes in practice location.

A specialty-specific policy adapts automatically to the insured’s medical field, so a resident entering a subspecialty fellowship keeps coverage aligned with that new specialty. Practice transitions, including a change of employer, do not affect the policy, and the coverage supports employment flexibility, including self-employed and locum arrangements group policies typically exclude.

For a resident with student loan obligations, this portability matters because loan payments remain due even during a disability. A policy that follows a physician from residency through fellowship and into practice keeps that protection in place exactly when career mobility is highest.