Physician Disability Insurance

Protecting medical professionals for over 30 years.

Disability Insurance Quotes for Doctors

Disability Insurance for Doctors

Own-occupation specialty-specific disability insurance plans for surgeons, cardiologists, neurologists, dermatologists, orthopedic surgeons, anesthesiologists, radiologists, pathologists, ophthalmologists, gastroenterologists, pulmonologists, oncologists, psychiatrists, obstetricians, and other medical specialists.

Customize Your Physican Disability Insurance Quote

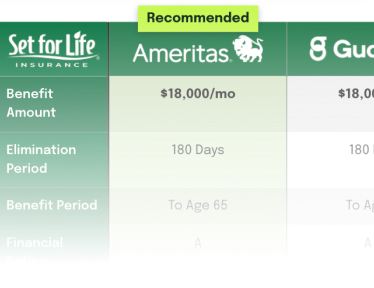

Compare Physician Disability Coverage Side‑by‑Side

Get Your Customized Physician Quote

"*" indicates required fields

She made updating my files with each life event stress-free. I watched colleagues struggle to communicate with insurance companies, but not me. One email to Jamie and everything is taken care of. My family is protected and done so with ease, all thanks to Jamie. I highly recommend Set For Life!!!

Physician Disability Insurance Brokers

How Physician Disability Insurance Works

Physician disability insurance protects your income if injury or illness prevents you from performing the material and substantial duties of your medical specialty. Unlike most employer group plans, an individual policy is personally owned, portable, and non-cancellable as long as premiums are paid.

When applying, insurers evaluate your specialty, income, and medical history to determine eligibility and benefit limits. A strong policy includes a monthly benefit amount, an elimination period, a defined benefit duration, and—most importantly—a true own-occupation definition tailored to physicians. Because medical careers are highly specialized, the structure of the policy should reflect how you actually earn your income.

High-income professionals across many fields rely on income protection coverage. In addition to physicians, dentists, and attorneys, specialized policies such as disability insurance for athletes are also used to protect professional sports income.

What to Look for in an Own-Occupation Policy

Not all own-occupation policies are structured the same way. Physicians should look for a true own-occupation definition that pays full benefits if you cannot perform your specialty—even if you work in another role.

Key features to evaluate include:

-

- True Own-Occupation Definition

-

- Residual or Partial Disability Rider

-

- Future Increase Option (FIO)

-

- Mental/Nervous Coverage Limits

-

- Non-Cancellable and Guaranteed Renewable Provisions

Physicians in procedural or surgical specialties should pay close attention to how the policy defines disability relative to hands-on patient care and surgical duties.

| Ameritas Life Insurance Corp. 4501NC · Enhanced Residual Rider (AERES) |

Guardian Berkshire Life Insurance Co. of America ICC16 18ID · Provider Choice + Enhanced Partial Rider |

Lloyd’s Petersen International Underwriters PDI111521 · Optional Residual Rider |

Mass Mutual Massachusetts Mutual Life Insurance Co. ICC15-XLIS-RC · Extended Partial Disability (EPR) |

Principal Principal Life Insurance Company ICC22-800-IDI · Income Protector |

The Standard Standard Insurance Company B180(7/17) · Platinum Advantage + Residual Riders |

|

|---|---|---|---|---|---|---|

| Income Loss Threshold That Triggers Residual Benefits | ||||||

| Minimum income loss required % of prior earnings that must be lost before residual benefits begin |

15% loss of monthly earnings (Specimen) One of the lowest thresholds available. Rider text states: loss must be “at least 15% of your prior monthly earnings” due to sickness or injury. |

Loss of Income due to disability (Specimen) Guardian’s Enhanced Partial rider defines “Loss of Income” as the difference between Prior Income and Current Income attributable solely to the Injury or Sickness. No explicit percentage floor in the base rider — benefit scales proportionally with income loss. Must be Gainfully Employed. |

Optional rider — threshold per rider terms (Specimen) Base Lloyd’s specimen (PDI111521) notes “Residual Disability is an optional benefit that only applies if the rider was purchased.” Rider text not included in this specimen. Typical Lloyd’s/PIU residual riders require income loss and inability to perform all material duties. |

20–80% loss of Predisability Earnings (Standard) EPR benefit is payable when Monthly Earnings fall to 20%–80% of Predisability Earnings. Below 20% earnings remaining triggers full benefit. Above 80% earnings remaining, no EPR benefit is paid. |

Loss of Earnings from own occupation (Specimen) Principal’s Residual Disability Benefit Rider requires a loss of Earnings due to Disability. The specimen confirms “Earnings” excludes unearned income. No explicit minimum percentage floor — benefit scales pro-rata with the earnings loss ratio. |

20% loss of Predisability Earnings (Enhanced); 15–20% for Short-Term version (Specimen) Specimen lists Basic, Enhanced, and Short-Term Residual riders. Enhanced Residual: benefit payable when Monthly Earnings are 20%–80% of Predisability Earnings. |

How Much Disability Coverage Physicians Typically Buy

Coverage amounts vary by income level and career stage. Residents and fellows often begin with smaller policies—sometimes through guaranteed standard issue (GSI) programs—while attending physicians typically structure coverage to replace a meaningful percentage of income.

High-income specialists may layer policies or increase coverage over time as earnings grow. The objective is to align protection with long-term income potential, tax treatment, and any existing group benefits—not simply to purchase the maximum available amount.

Ready to compare? Jump to the quote request form.

| Ameritas Life Insurance Corp. 4501NC · Enhanced Residual Rider (AERES) |

Guardian Berkshire Life Insurance Co. of America ICC16 18ID · Provider Choice + Enhanced Partial Rider |

Lloyd’s Petersen International Underwriters PDI111521 · Optional Residual Rider |

Mass Mutual Massachusetts Mutual Life Insurance Co. ICC15-XLIS-RC · Extended Partial Disability (EPR) |

Principal Principal Life Insurance Company ICC22-800-IDI · Income Protector |

The Standard Standard Insurance Company B180(7/17) · Platinum Advantage + Residual Riders |

|

|---|---|---|---|---|---|---|

| Monthly Benefit Calculation Formula | ||||||

| Residual benefit formula How the monthly residual check is calculated |

Residual Monthly Benefit = (Loss of Monthly Earnings / Prior Monthly Earnings) x Base Monthly Benefit (Specimen) First 6 months minimum: The greater of (a) 50% of base monthly benefit OR (b) the formula result. 75%+ loss rule: If loss exceeds 75% of prior monthly earnings, treated as 100% loss and full base benefit is paid. Prior earnings: Average of highest 12-month or 24-month period before disability, indexed annually for CPI-U after year 1. |

Partial Disability Benefit = (Loss of Income / Prior Income) x Monthly Benefit (Specimen) Prior Income: Average monthly income for either (a) last 24 calendar months, or (b) the two calendar years with highest earnings in the three years before disability — whichever is greater. Current Income: All income for services during disability, excluding pre-disability earned-but-not-yet-received income. Full benefit floor: If loss of income is 100% or more of Prior Income, full monthly benefit is paid. |

Proportional formula — rider required (Specimen) Rider language not included in this specimen. Lloyd’s/PIU residual riders typically use a proportional income-loss formula: (income loss / pre-disability income) x base benefit. Confirm with current rider filing. |

EPR Benefit = [(Predisability Earnings – Monthly Earnings) / Predisability Earnings] x Monthly Benefit (Standard) Full benefit if earnings are less than 20% of predisability earnings. No benefit if earnings are greater than 80% of predisability earnings. Prior earnings: Average of the 24 months before disability began. |

Residual Benefit = (Loss of Earnings / Prior Earnings) x Maximum Monthly Benefit (Standard) Prior Earnings: Average monthly Earnings for the 12 months before disability. Current Earnings: Earnings during the disability period, excludes passive/unearned income. Minimum benefit: Typically 50% of base benefit for first 6 months. |

Residual Benefit = [(Predisability Earnings – Monthly Earnings) / Predisability Earnings] x Basic Monthly Benefit (Standard) Full benefit trigger: If Monthly Earnings are less than 20% of Predisability Earnings, full Basic Monthly Benefit is paid. Basic Residual Rider: Flat 50% of base benefit when qualifying criteria met. Enhanced Residual Rider: Proportional formula above; includes Recovery Benefit. |