Overhead and insurance costs have climbed to the top of dentists’ business concerns entering 2025, according to the American Dental Association Health Policy Institute. Dental practice owners cite rising operating expenses, staff payroll costs, and higher insurance premiums as the most persistent financial pressures.

Employer family health-plan premiums rose six percent in 2025 to an average of US $26,993, according to the KFF Employer Health Benefits Survey. Those higher premiums add to fixed-cost burdens across private practices and hospital-based dental groups alike.

Musculoskeletal strain is another major source of occupational risk. Work-related musculoskeletal disorders affect nearly all dental professionals—at least 96 percent, according to a 2025 study in Frontiers in Rehabilitation Sciences—illustrating how physically demanding clinical practice has become. “Dental practitioners are at risk for repetitive strain injuries due to activities such as gripping and using slender instruments repetitively,” wrote Dr. Erica Kholinne and colleagues.

Diagnosis and occupational class continue to shape disability-insurance pricing, Society of Actuaries research shows, leaving oral surgeons—whose livelihoods depend on fine-motor precision—among the highest-risk categories in the market. But financial pressure is only part of the story.

Surgeons Feel the Strain as Physical Risks Tighten Insurance Costs

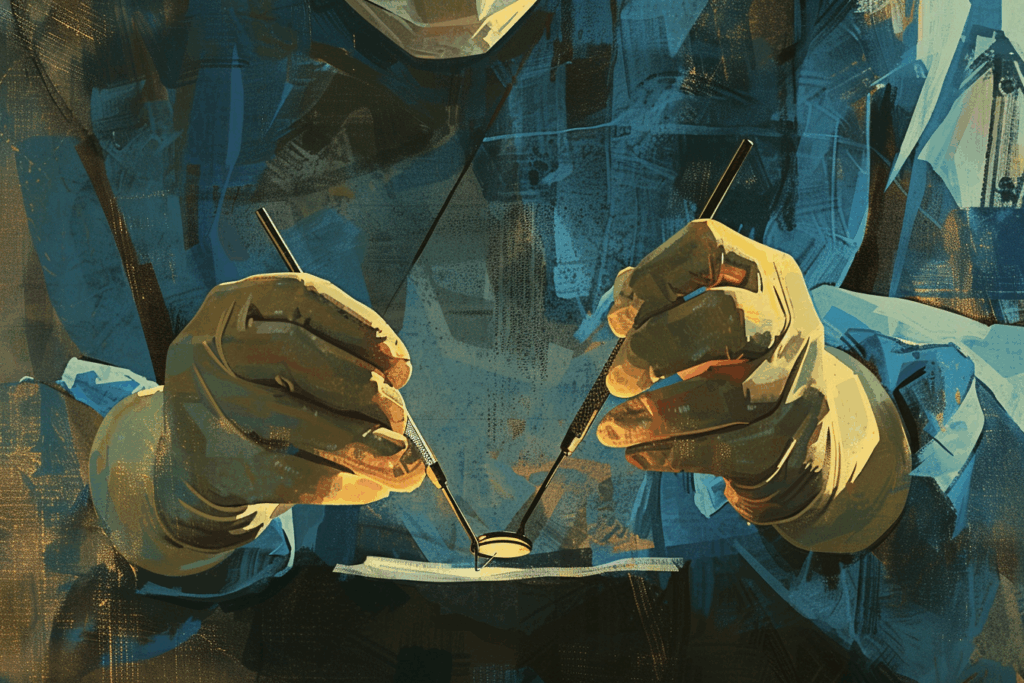

Oral and maxillofacial surgeons spend hours each day bent over operating tables, relying on precise muscle control and posture. Even a mild tremor, wrist injury, or neck strain can force an extended absence. That physical vulnerability now mirrors an economic one.

Because premiums rise with occupational risk, oral surgeons pay some of the steepest disability-insurance rates in healthcare. Policies typically cost between 1.5 and 3 percent of annual income—or roughly US $3,000 to US $9,000 per year for a specialist earning US $300,000. Optional riders such as cost-of-living adjustments or residual-income protection can add 20 to 40 percent more, but many surgeons consider those features indispensable in an unpredictable market.

This combination of physical strain and financial exposure has pushed more specialists to evaluate their coverage structures carefully.

Own-Occupation Policies Gain Ground as Surgeons Seek Stability

Coverage definitions often determine whether a claim is approved or denied. Under an own-occupation contract, a surgeon unable to operate because of injury or illness can still collect full benefits while working in another capacity, such as teaching or consulting.

Claim outcomes vary widely across medical specialties, with diagnosis and occupation remaining key factors, research from the Society of Actuaries Individual Disability Experience Committee shows. The findings highlight why disability Insurance for dentists has become a core consideration for oral and maxillofacial surgeons seeking income stability in high-risk specialties.

Many practitioners have shifted toward own-occupation policies since 2020 for added flexibility amid changing health and economic conditions.

Overhead Coverage Emerges as the Safety Net for Private Practices

For surgeons who own private practices, disability disrupts more than income. Rent, payroll, and equipment financing continue regardless of medical status. Business Overhead Expense (BOE) policies have become vital companions to personal coverage, reimbursing fixed business costs for 12 to 24 months and allowing time to recover or sell the practice.

Overhead and insurance issues now rank among the top challenges for practice owners, the ADA Health Policy Institute reports. Nearly four in ten dentists increased borrowing in 2024 to cover equipment and labor expenses—debt that heightens financial risk if operations pause. Insurers increasingly weigh that debt load when pricing BOE and supplemental riders.

Surgeons Layer Coverage to Safeguard Income and Practices

Many oral surgeons are combining personal disability insurance with business-overhead coverage to maintain both income and practice solvency during extended recovery periods. The approach ensures that household finances remain stable while operating costs—like rent, payroll, and loan payments—are reimbursed through a separate policy. Industry advisers say this layered model is becoming a standard safeguard for high-risk medical specialists in 2025.

Layered coverage also offers long-term flexibility. Surgeons who purchase both types of policies can often adjust benefit terms as their practice structure or income changes—a feature that has grown more valuable as private practices consolidate and multi-location groups expand. Analysts say this adaptability helps specialists weather not only medical leave but also broader shifts in the healthcare economy.

Fine-motor injuries push more surgeons toward own-occupation disability coverage in 2025. [VIDEO]

Insurers Tighten Rules as 2025 Brings Longer Claims and Higher Costs

Longer claim durations and inflation-adjusted benefit structures have led insurers to tighten underwriting standards across the disability-insurance market. Diagnosis-specific claim patterns and occupational risk levels remain the main pricing drivers, according to the Society of Actuaries’ 2024–2025 Individual Disability Insurance studies.

To counter rising rates, dental-school networks and professional associations are expanding group-rate and unisex-pricing programs. These arrangements can reduce premiums by 10 to 25 percent without changing coverage definitions. Participation has grown fastest among early-career specialists and women surgeons, who previously faced steeper gender-based pricing.

Once enrolled, the reduced rate often remains locked even after a job change—if the policy converts to individual ownership. That portability has become a major advantage for surgeons balancing academic, hospital, and private-practice roles.

Balancing Group Coverage with Long-Term Guarantees

Group disability plans offer short-term affordability but limit control. Coverage usually ends when employment does and caps benefits at 60 percent of income. Individual contracts secure lifetime rate guarantees under non-cancellable, guaranteed-renewable terms.

Tax treatment differs: benefits from employer-funded plans are taxable income, while benefits from personally funded policies are tax-free, according to the IRS Guide to Business Expense Resources.

“New cases of chronic pain occur more often among U.S. adults than new cases of several other common conditions, including diabetes, depression, and high blood pressure,” the National Institutes of Health reported in 2024. The agency found that chronic pain often continues for a year or longer, reinforcing why layered disability protection—through both personal and business-overhead coverage—has become essential for oral surgeons facing long recovery periods.

Specialization Offers Stability Amid 2025 Insurance Volatility

Analysts expect disability-insurance premiums to stay elevated through 2025 as carriers adjust to claim trends and inflation-linked benefits. Yet institutional discount programs through universities such as Harvard, Penn, Columbia, and Michigan continue to expand, offering oral-health professionals access to unisex-rated, portable plans that stabilize long-term affordability.

For oral surgeons whose livelihoods depend on surgical precision, disability coverage has evolved from a financial safety net to a professional necessity. The conversation has shifted from whether to how comprehensively to insure against the unexpected.